Do THIS to know if your pricing model is helping or hurting you

Figure 1: How good is your pricing model?

You may be wondering how "good" your pricing model is. You may have poor results and wonder if you should invest to improve pricing. Or you have great results but wonder if you should tweak your model to continue to generate returns. Or you may see competitors charge significantly less but report good results, and you wonder if you are missing a trick.

To answer any of these questions, the first thing to do is to measure the performance of your current pricing model.

Why measure the performance of your pricing model?

You want to measure the performance of your pricing model because:

If you have poor results, and the performance of your pricing model is also poor, then you can drill down and see what parts of the model are driving those poor results and create an effective plan to improve pricing.

If you have good results, the performance of your pricing model is also likely to be good. Measuring performance is still worthwhile for two reasons (a) it may identify areas for more profitable growth, and (b) it allows you to see how investments in your pricing model improve its performance.

How is a pricing model “good”?

A pricing model provides a premium made up of three parts (1) a loss prediction for that particular policy (2) expenses and (3) profit. To measure the performance of a pricing model, we are comparing how accurate the loss prediction is (part 1) when compared to the actual ultimate loss for that policy, for the book of business you have actually written.

But we can’t do this for individual policies - there is too much volatility in insurance to be predictive on an individual policy level. Instead, we first group policies into those where you have a low loss prediction per exposure, and those with a high loss prediction per exposure, and analyze how the predicted and actual ultimate losses align by group.

A “good” model has predictions that closely align with actual loss and also successfully differentiate between high-loss versus low-loss exposures.

What actions can you take after measuring the performance of your pricing model?

Let's look at the fictional performance of an auto carrier in Figure 2 below. In bucket 1 are the policies that the pricing model predicts will generate the lowest loss per vehicle year, and in bucket 5 are the policies that the pricing model predicts will yield the highest loss per vehicle year.

OBSERVATION: In bucket 1, there are policies that the pricing model predicted would have $434 in losses per vehicle year. However, these policies performed even better, generating only $312 in ultimate loss per vehicle year.

ACTIONS: Bucket 1 is an opportunity for profitable growth. The carrier should understand the customer characteristics for this bucket and target these customers.

OBSERVATION: In bucket 5, the pricing model predicted $1,033 in losses, but the actual losses were 18% higher, at $1,244 per vehicle year. The loss ratio for this bucket will also be 18% higher than expected.

ACTIONS: Understanding the types of policies in this bucket may explain why they are underpriced and how to correct this. It can also point to changes you can make to risk selection and underwriting.

Figure 2: Example pricing model performance for a fictional auto carrier

I'm sure someone checked model performance when they build the model. Why should I do this again?

You may think there's no need to check the performance of your pricing model because this was done when the model was built.

While it is good practice to check the model performance when building the model, it is also a good idea to continue doing this after you've deployed your pricing model to check that it's still working. The model may look good when it's built but perform poorly after it's deployed. Typically, this is because the underlying drivers of loss may have changed, or your book of business may be shifting.

Get the Step-by-step guide on how to measure pricing model performance

Get our simple step-by-step guide on how to measure pricing model performance. It’s free, and you don’t need to be an actuary to follow along.

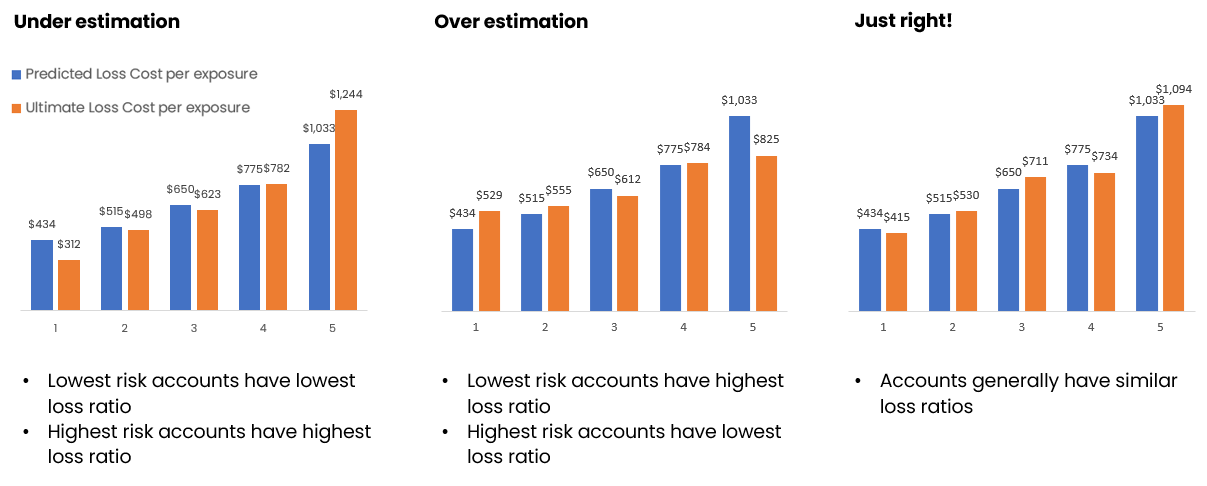

What are the three different results I might see?

In practice, your pricing model performance is likely to show one of three different results: under-estimation, over-estimation or be just right.

Figure 3: Three different results from measuring your model performance

Under-estimation. This is when your lowest-loss accounts have the lowest loss ratio, and the highest-loss accounts have the highest loss ratios, as in Figure 1 above. Here is what you can do if you see this:

The policies in bucket 1 represent opportunities for profitable growth, and the unprofitable policies in bucket 5 represent opportunities for risk selection and revisiting pricing.

Under-estimating could occur if you are overly aggressive at capping the model prediction. For example, your pricing model may have predicted a lower loss cost in bucket 1; however, you may have created a rule to constrain the discount it could give. You can now revisit this decision and consider relaxing these constraints, which can lead to capturing more opportunities in bucket 1 and correctly pricing for accounts in bucket 5.

Over-estimation. This is when your lowest risk accounts in bucket 1 have the highest loss ratio because although the ultimate loss was low, it did not turn out to be as low as the pricing model estimated. Conversely, the highest-risk accounts in bucket 5 have the lowest loss ratios. Taking action is more challenging in this scenario:

You may have a strategy to attract the lowest-risk accounts, which are in bucket 1. Since bucket 1 accounts have the highest loss ratio, consider revisiting this strategy.

This result is a sign to revisit your pricing model. If you don't have a predictive pricing model, then the rigorous, multi-variate analysis this involves has a good chance of fixing the issues in this scenario.

Just right. If your predicted and ultimate loss costs line up well for all buckets, and there is a good slope in your graph, showing good differentiation between high and low risk, your model is performing well. A few things to note:

Your competitors may have a similar graph but with more slope than yours. For example, while you can identify accounts in bucket 1 with an ultimate loss of $415, they may be able to reliably identify accounts that only generate an ultimate loss of $200. In this case, they will win those accounts and grow profitably at your expense.

Therefore, even if you have a pricing model that looks to perform well, you may still want to look for opportunities for improvement. And you are now armed with the ability to see how well potential improvements move the needle on model performance.

Gain competitive advantage by measuring the performance of your model

In our experience, few carriers and MGAs regularly assess their pricing model performance after the model has been deployed. Even in this world of AI and Insurtech, this simple analysis can give you some competitive advantage. I encourage you to try it and see whether it can highlight areas of opportunity and areas of poor performance to address.